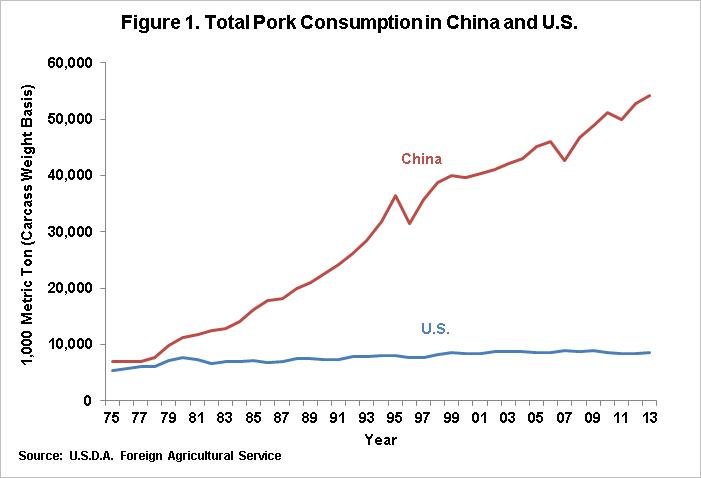

China’s enduring appetite for pork is legendary, but recent years have brought a discernible shift: the nation’s consumption of this staple protein appears to be reaching a saturation point. For decades, pork enjoyed pride of place in Chinese culinary habits, woven into everyday meals and elaborate banquets alike. With greater urbanization and rising incomes during the early 2000s, per capita consumption surged alongside rapid expansion in domestic production capacity—a trend long considered almost inexhaustible.

Last year marked a curious inflection. Official data indicates that China produced about 57 million tonnes of pork in 2024—a figure down roughly 1.5% from the prior annum—owing initially to disease-induced herd liquidation and financial woes among smaller-scale producers who exited sow production for more short-term ventures like fattening pigs or abandoning livestock altogether. Efficiency-focused large farm operators kept sow herds stable by ruthlessly culling unproductive animals while concentrating on yield optimization, leaving little room for extensive growth spurts reminiscent of past booms.

Pork remains king; even so, demand has softened recently despite mid-year price upticks driven by supply disruptions. The marketplace has become notably cautious: large-scale actors pursue profit margins through scale and technological integration rather than chasing higher output per se—emblematic of an industry confronting physical as well as economic ceilings.

In Q1 2025 total meat production increased modestly to reach approximately 25.40 million tons in aggregate (up just about two percent year-on-year), with pork registering only a mild gain near 1.2%. The nationwide pig population expanded slightly by around two percent as well; numerous smallholders continued departing amid stiff competition from vertically integrated conglomerates possessing deeper pockets and superior risk management capabilities.

Curiously enough though—the number of slaughtered pigs remained nearly unchanged compared to last year; productivity improvements resulted mostly from greater carcass weights instead than headcount expansion alone (in contrast with typical previous cycles where aggressive restocking often fueled recovery phases after disease outbreaks). Sometimes statistics seem paradoxical at first glance—increased live animal numbers didn’t immediately translate into materially higher slaughter rates—which observers attribute partly due to more judicious batch finishing coupled with stricter biosecurity protocols now commonplace post-African Swine Fever era.

Imports tell their own intriguing story too: pigmeat imports have fallen steadily over four consecutive years up through Q1 2025—even as offal shipments grew apace—shedding light on evolving consumer preferences away from muscle cuts toward specialty items prized for both tradition and economy alike within many provincial markets outside major urban cores. Geopolitical tremors cast an uncertain pall over prospects for future foreign sourcing; unresolved trade actions targeting EU-origin pork continue hovering ominously overhead while market participants attempt hedging against potential tariff escalations or other unforeseen impediments affecting global flows into China.

Price pressure persists across segments despite sporadic bouncebacks during peak holidays such as Lunar New Year when families still favor lavish feasts replete with classic dishes starring various rendered parts of the hog—from belly and trotters down to esoteric organ meats rarely featured elsewhere globally but imbued here with centuries-old cultural cachet not easily replaced by imported alternatives or newer proteins like plant-based analogues that, albeit trendy regionally among affluent youth demographics especially in Beijing or Shanghai districts where international exposure runs high enough already influencing lifestyle experimentation more rapidly than conservative rural heartlands could ever countenance.

Production cost curves finally trended downward this past fiscal cycle largely thanks binding input expenses amelioration—feed grain prices stabilized following tumultuous spikes seen earlier—and government-backed efforts fortifying disease prevention infrastructure paid clear dividends via enhanced herd health metrics overall (though lingering pockets remain vulnerable wherever lax oversight allows resurgent pathogens any natural foothold).

Forward-looking analysis suggests status quo holds barring unforeseen supply-side shocks: Rabobank foresees domestic output remaining relatively stable at close-to-2024 benchmarks throughout coming months even if consumer sentiment demonstrates ongoing reticence toward incremental increases absent broader macroeconomic optimism—a somewhat meandering trajectory given recent history rather than sharp cyclical rebounds common previously following adverse supply corrections caused either policy missteps or sudden epidemiological jolts taken together implausibly recurring too often given tighter controls nowadays generally reduce such risks significantly versus five years ago before ASF upended everything so profoundly overnight it sometimes seemed nothing would ever recover fully again yet gradually things found equilibrium anew all the same eventually albeit never quite returning absolutely normalcy people remembered before crisis gripped sector whole-cloth originally circa late-2018 period when panic first spread quickly enough cause lasting reforms impossible ignore any longer no matter how entrenched old habits may once have seemed invulnerable amid explosive demand growth decade prior that era now looks increasingly unlikely repeat itself anytime soon under current regulatory regime constraints plus maturing consumer profile shifts underpinning transition towards plateaued aggregate intake baseline grounded real-world spending power realities superseding mere dietary aspiration alone previously held sway unfettered fashion across wide swath country simultaneously without caveats otherwise provisos mitigating pace transformation latterly observed instead nowadays everywhere you look almost invariably true whatever local specifics might dictate case-to-case basis diverging outcomes won’t wholly erase big-picture narrative widely recognized shaping future contours industry domestically going forward indefinitely not just short term horizon anybody currently investing substantial resources ought bear firmly mind thus recalibrating strategies accordingly lest strategic misfire prove costly down line unexpectedly after all calculations are completed ultimately regardless best intentions involved should circumstances suddenly alter course unpredictably thereafter rendering certain measured bet less advantageous hindsight scrutiny might reveal retroactively if lessons hard-won forgotten sooner than prudence advises one thinks too far ahead sometimes missing wood trees situation demands careful vigilance above anything else pragmatically speaking anyway until some new pattern supplant prevailing stasis sets motion once more naturally arising perhaps decades hence when today’s seeming certainty seems quaint relic another age entirely whose outlines faded irretrievably except archival record memory preserves sparingly reluctant surface nostalgia barely hints deeper causes underlying contemporary moment lived out day-by-day purposefully reluctant indulge easy answers resolving persistent ambiguity enterprise scale unique so singular few precedents anywhere match scope challenge posed regionally let alone universally accepted solutions already at hand everyone admits must still invent themselves inevitably moving onward nevertheless endures resiliently somehow beyond easy computation means .